Profits come from service diversification

Looking at the profit results of the four State-owned commercial banks (Big 4), Vietcombank had a pre-tax profit of nearly VND23.1 trillion (approximately US$1 billion) - the highest level in the banking system, helping the lender to be in the list of 200 groups with the highest profit in the world. Vietcombank's credit growth in 2020 was higher than the general growth rate of the banking system, at 14 percent. This is also the highest credit growth ever of this lender and the highest in the banking industry.

The pre-tax profit of Vietinbank also reached VND16.45 trillion, up 43.5 percent over the previous year due to good credit growth. The recent report of Agribank shows that not only did the business results continue to improve, Agribank's administrative costs in 2020 were also being cut by 10 percent, helping the bank's pre-tax profit to touch nearly VND12.87 trillion, VND369 billion, or approximately 3 percent, higher than the plan. It was eligible for the State budget to allocate VND3.5 trillion to increase its capital. Among the Big 4, only BIDV saw a decrease in profit last year, with a consolidated pre-tax profit of roughly VND9.02 trillion.

Not only State-owned commercial banks but joint-stock commercial banks also saw a sharp increase in profits. Specifically, MSB announced that its profit in 2020 jumped by 94 percent compared to 2019. ABBank's profit was more than VND1.4 trillion in 2020, exceeding more than 100 percent of the annual plan, much higher than its profit plan.

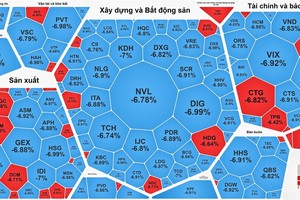

The bright picture of the banking industry's profits is also the reason why banking stocks became king stocks again on Vietnam’s stock exchange last year. The majority of banking stocks have increased from 50 to more than 100 percent. Even some banking stocks have increased by 200 percent compared to the beginning of last year.

According to Dr. Can Van Luc, Chief Economist of BIDV, with the average inflation rate at 3.23 percent last year, the fact that depositors received a one-year interest rate of 5.5 percent-6 percent is not low. The difference of 2.5 percent in the interest rate of the input (savings deposit interest rate) and output (lending interest rate) of the banking system is low compared to the average of 3 percent of the region.

It shows that the bank profits have been coming from an important part in which banks have diversified products and services, especially the retail service segment related to digital banking. Many other new services have been taking shape and developing faster in recent years. Although the provision for bad debt increased, partially affecting the bank profits, thanks to diversifying the revenue sources, especially non-interest income sources, bank profits remain optimistic.

Credit expansion goes with safety and efficiency

According to SBV Governor Nguyen Thi Hong, last year, the State Bank has reduced the operating interest rate three times, with a total reduction of 1.5-2 percent per annum. With the above operating policies and the direction of saving costs to credit institutions, the current highest deposit interest rates at banks are from 6.5-7.1 percent per annum, with a term from 12 months upwards. The average lending interest rate in 2020 decreased by about 1 percent on average compared to the end of 2019.

Accordingly, the maximum short-term lending interest rate in Vietnamese dong for some industries and sectors was at 4.5 percent per annum. Governor Nguyen Thi Hong assessed that this year, the Covid-19 pandemic would possibly continue to be complicated, and the prospects for the global and domestic economies remained unpredictable, so the banking industry would continue to implement measures to remove difficulties for enterprises and people. Credit expansion must go with safety and efficiency.

Dr. Can Van Luc analyzed further that although the banking system reported profit growth of about 10 percent over the same period last year, this figure failed to show the true nature of the profits in the banking system. Because last year, SBV’s Circular No.01/2020 allowed the banking system to restructure its debts, but still keep the same group of debts instead of changing the group, so there was no need to make provisions for risks.

This year, the SBV, as well as the Ministry of Finance, has proposed the Government to amend Circular No.01/2021 in the direction of requiring credit institutions to make provisions for risks, with a roadmap of about three years. As a result, this year will actually reflect the profits of the banking system. Accordingly, profits are expected to only increase from 8 percent to 10 percent this year, not as strong as before.

As for commercial banks, Mr. Nghiem Xuan Thanh, Chairman of Vietcombank's Board of Directors, said that the banking industry's profits increased sharply, so it is reasonable to ask banks to lower interest rates. However, in the past time, Vietcombank had reduced interest rates in its whole system, meaning that any enterprise or individual directly and indirectly affected by the Covid-19 pandemic received a 1-percent and a 0.5-percent decrease, respectively, in interest payment. Everyone enjoyed interest rate reduction.

Currently, Vietcombank's lending interest rates are the lowest in the market, but the lender still has room to lower its rates further because its provision is quite high. However, if it continues to lower interest rates, enterprises with excellent business performance will flock to Vietcombank, causing difficulties for other credit institutions.

The SBV should not impose a general administrative order on interest rate reduction, but sit with commercial banks to know how the lending interest rate of each bank is and adjust it properly, Mr. Thanh proposed.

However, an expert noted that if banks give loans carelessly, causing provision to increase due to bad debts, the profits will be eroded immediately. Banks that have lowered interest rates but their profits still increase are those with good business.

In fact, some commercial banks have reduced their profits by trillions of Vietnamese dong through lowering interest rates to support and accompany customers to overcome the Covid-19 pandemic, such as VietinBank and Vietcombank.